Indian Speciality Chemicals industry is worth USD 30 billion and forms 20% of the Chemicals Industry. Indian speciality chemicals grew 2x global speciality chemicals at CAGR of 13% over FY10-18 and is likely to grow at 14% per annum. It is expected to accelerate to 17% driven by domestic growth and stable exports. The growth drivers of Speciality Chemicals are 1. Increased End use Domestic Demand, 2.Strong Export Demand, 3. Mergers and Acquisitions on rise, 4. Cost Competitiveness, 5. Availability of skilled labour and 6. Investments in R&D. INR depreciation is also driving developed nations to shift/ start their operations in India.

Speciality Chemicals are a group of relatively high value, low volume chemicals known for its end use performance enhancing application. They are recognized for their ‘function’ rather than their ‘specifications’ as in the case of basic chemicals. They provide solutions to customer application, are knowledge based and known to deliver much more returns as compared to Base Chemicals.

The below exhibit show the key players in Indian Speciality Chemicals space covered on DistrictD platform.

Construction Chemicals, Paints & Adhesives and Consumer Chemicals are a huge sector in itself and are covered in the blogs to follow.

Speciality Chemicals are used to add value to end products and therefore industry operates on B2B Premises. Speciality Chemicals include diverse range of products and application to various sectors ranging from Flavours and fragrances, Colorants and Dyes, Homecare surfactants, Paper Chemicals, Printing Ink, Agri-chemicals, Coatings, Sealants and Elastomers. The end use industries for Speciality Chemicals include Automotive, Electronics, Fibre and Textiles, Food, Homecare, Agri-chemicals, Paper etc.

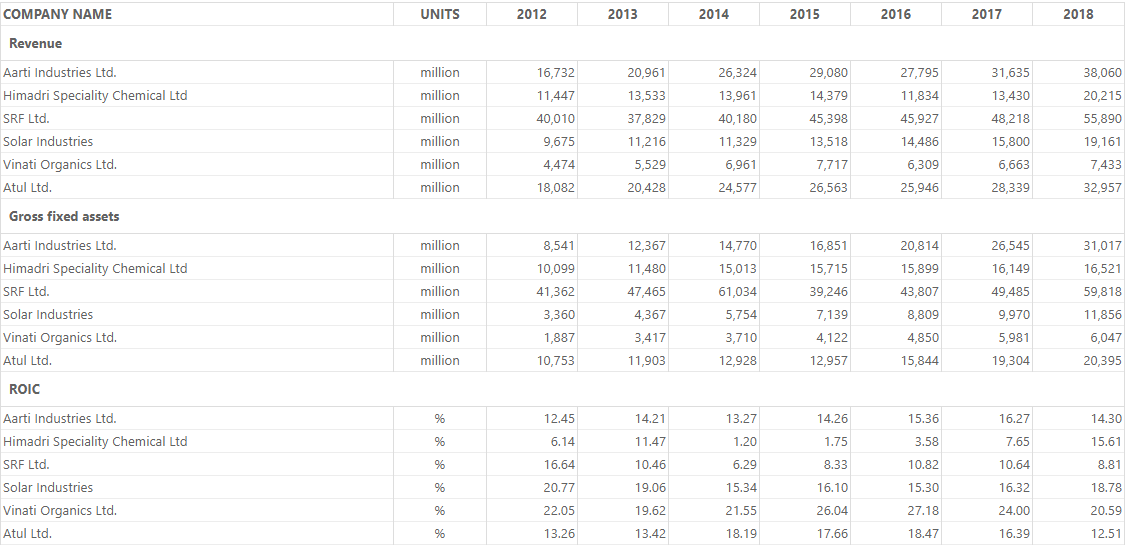

The table below shows the financial metrics of top Speciality Chemical manufacturers in India. Agri based speciality chemicals are covered in the latter half of this blog.

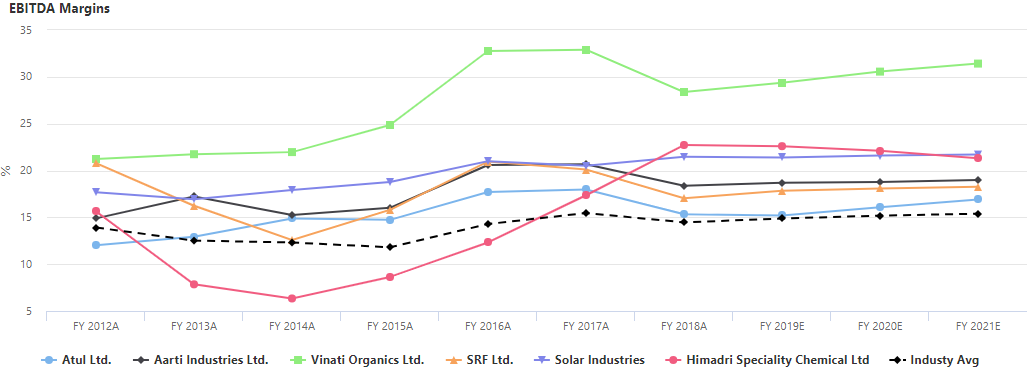

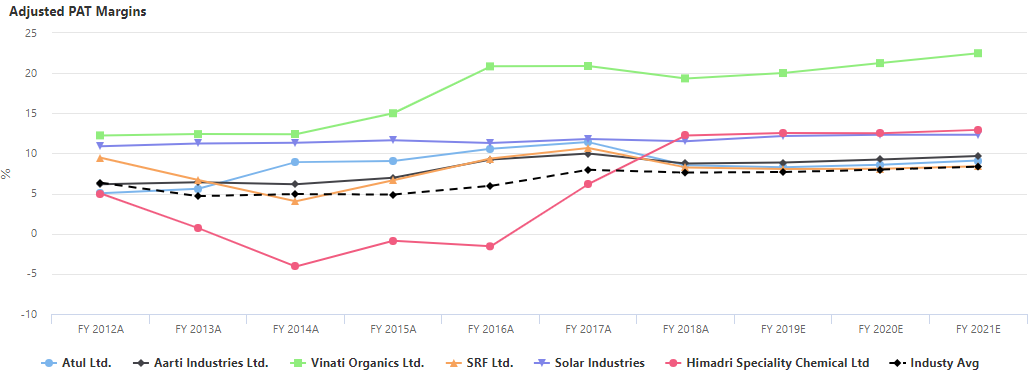

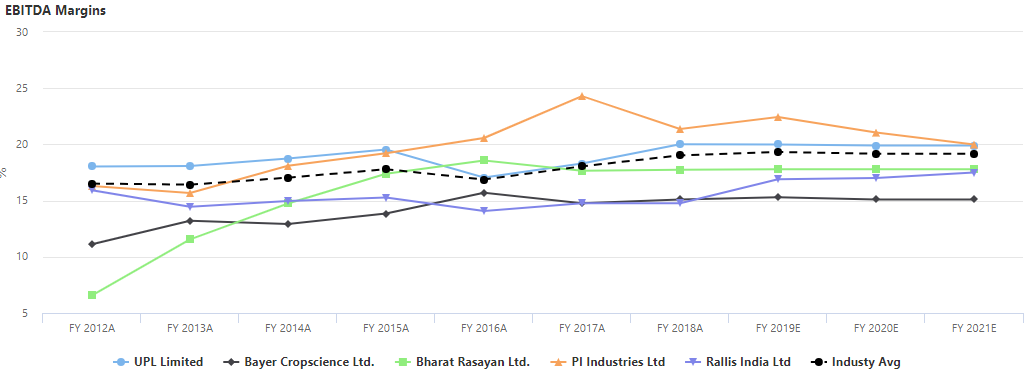

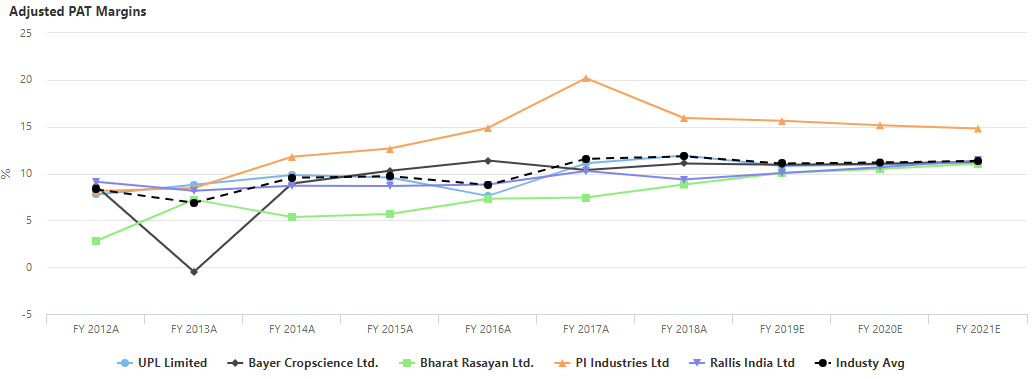

Apart from above mentioned players, BASF, Jayant Agro, Linde India, Clariant Chemicals, SH Kelkar etc are few eminent players in the speciality chemicals space. The charts below shows the margins and profitablity for the Speciality Chemical players.

*Industry Average includes ATUL, AARTIIND, CLNINDIA, KIRIINDUS, VINATIORGA, SRF, SOLARINDS, JAYAGROGN, BASF, HSCL, SHK.

Speciality chemicals are known to deliver stronger returns. The profit margins in Speciality Chemicals tend to be more stable since they show moderate degree of sensitivity to global economic growth when compared to Base Chemicals where margins are largely dependent on commodities. Because of their differentiated and value added nature, many product lines tend to enjoy higher and sustained profitability levels. Also asset turnover is lower i.e. ~1 for most of the Speciality Chemical companies.

SRF Ltd– Rapid progress made in high margin fluoro speciality and refrigerant gasses drive value growth. Speciality Segment forms 39% of its total revenue and grew at CAGR of 18% (FY 14-18) stood at Rs.1826crore. On the other hand, steady cash flows from technical textiles also supplement capacity expansion in fluoro speciality. SRF has delivered Revenue growth ~16% (2017-18) with EBITDA Margins 17% in FY 2018. Its speciality chemicals operations would be the growth engine in the times to come.

Aarti Industries– is the largest producer of Benzene derivatives in India and has emerged as one of the leading manufacturers globally. Its global market share in speciality segment in ~45%. Aarti has delivered Revenue growth 20.3% (2017-18) with EBITDA Margins ~18% in FY 2018. I further believe that company’s successful track record in expansion projects over recent years and its on-going capex can surprise growth positively.

Another application of Speciality Chemicals is to Agri-business. Speciality chemicals having a unique function, promotes agri-manufacturing, technologies and related services.

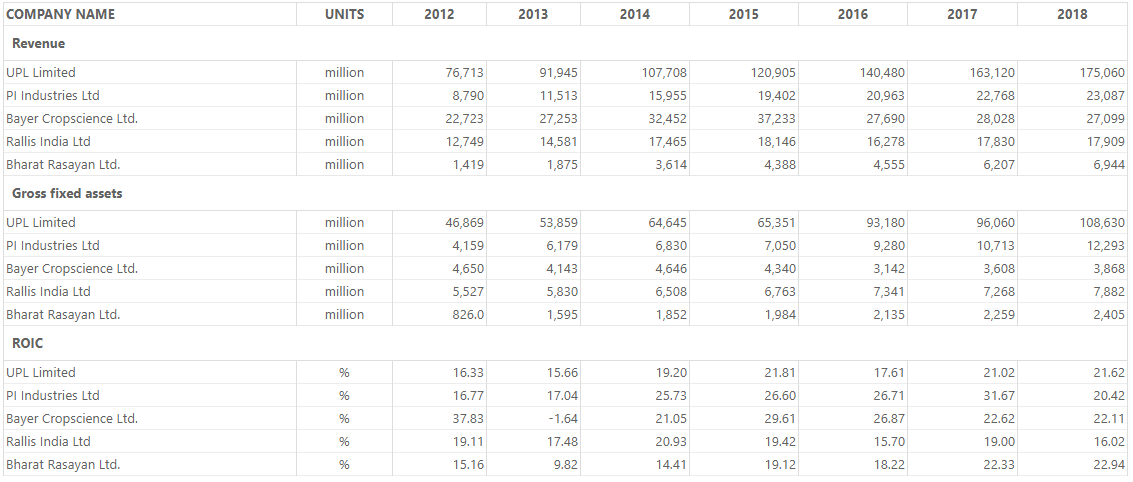

India is the fourth largest producer of agro-chemicals globally after US, Japan and China. At 157.35 million hectares, India holds 2ND largest agricultural land in the world. Indian agro-chemical industry stood at USD 4.7 billion in FY16 and is estimated to grow at CAGR of 7.5% to reach USD 9 billion by FY 24. The table below shows key financial metrics of top players in Speciality Agri-chemical sector.

The top 10 players in agro-chemical industry holds >85% of market share.

*Industry Average includes UPL, BAYERCROP, BHARATRAS, PIIND, RALLIS, SHREEPUSHK, BHAGIRADHA.

The mentioned players show above average ROIC with stable EBITDA Margins. Indian agro-chemicals companies continue to grow ~8% domestically and ~10% in exports due to 1.Increase in Rural spending 2. Lower Research and manufacturing cost. 3. Rise in Technically skilled manpower and products going off-patent. With agro-commodity prices looking up in export markets like Latin America (1/3rd of Indian agro-chemical exports), coupled with fall in exports from China, sector is expected to grow ~10% exports revenue.

United Phosphorous Ltd.– is India’s largest agro-chemical companies with 80% exposure to exports. UPL has seen revenue growth of 7.3% and EBITDA growth of ~18% (FY 17-18), is outperforming its peers. The growth drivers for UPL are 1. Balanced presence across products, segments and crops, 2. Robust presence in High growth countries such as India, Brazil (has a market of Rs.5000 Crore in Brazil and in process of setting up a unit in U.S.), 3. Presence across value chain with minimal dependence on outsourcing. The long term financial performance of UPL within the industry is good.

Looking Ahead

The Chemical Industry is a catalyst to economic development. The entire world depends on the multitude of products manufactured by chemical industry so the demand is constant. However huge capital requirements, patent protection and fragmentation within the sector leading to internal rivalry is a major challenge. But for every challenge there is equal opportunity. India is currently well positioned to take advantage of global chemical sector focus shifting towards east.

**The charts and tables in the blog are made using DistrictD platform.

Related Blogs

CUSTOMER TEACHINGS, PROBLEMS AND US

Most of what I previously wrote was from our point....

Udit Garg

08/06/2022 11:34 AM

Fundamentals, Test Match

Hope you grabbed one of the biggest opportunities ....

Priyanka Gandhi

31/05/2022 04:41 PM